Form 5471 Penalties

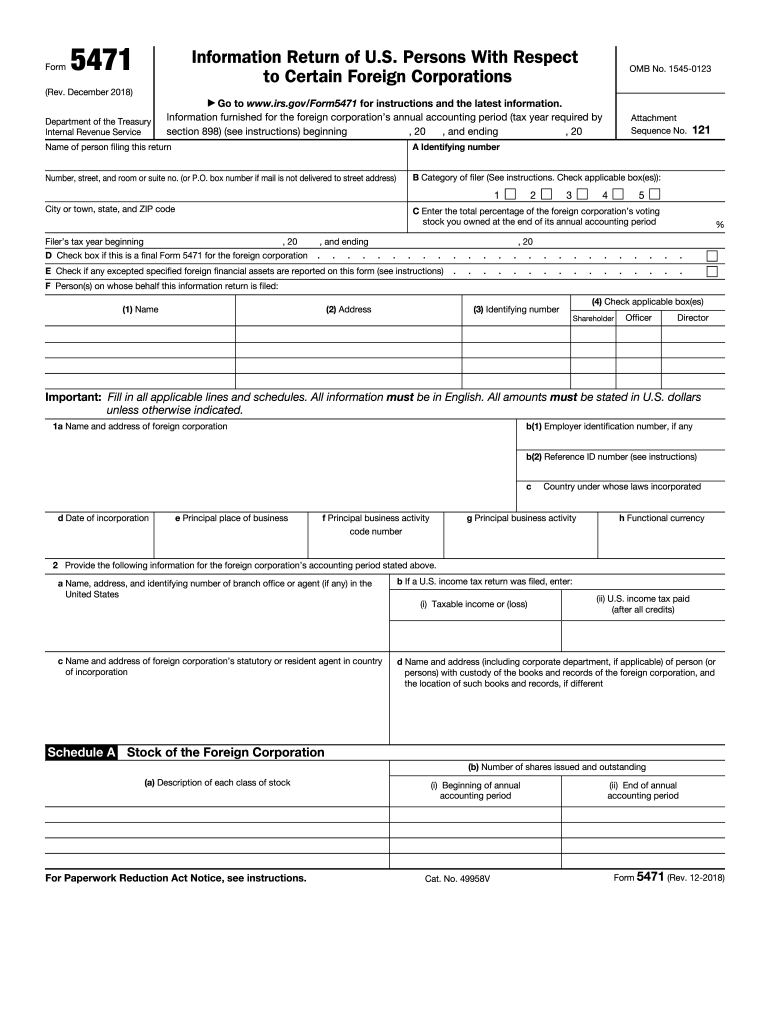

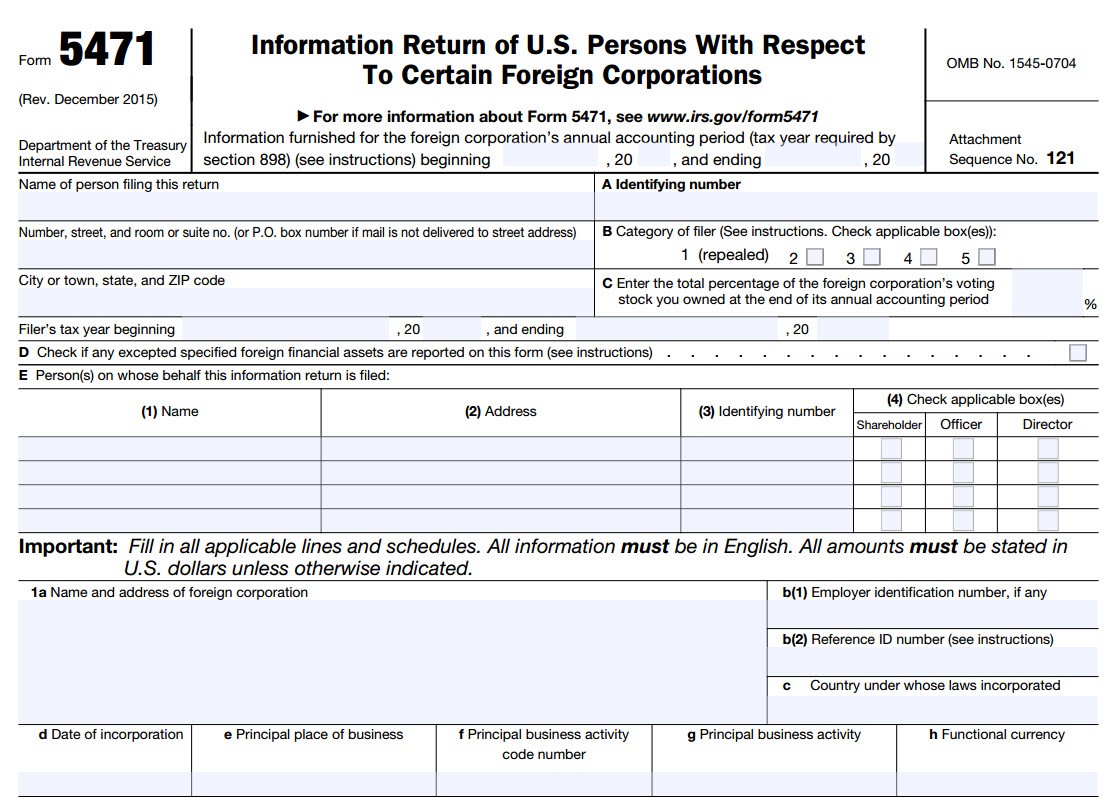

Form 5471 Penalties - Web in response to the taxpayer’s failure to file forms 5471, the irs imposed $10,000 per year in initial penalties under section 6038 (b) and $50,000 per year in continuation penalties for the tax years 2003 through 2010. (9) irm 20.1.9.4.4 — updated to account for the repeal of irc 902, which was part of the tax cuts and jobs act. Criminal penalties may also apply for failure to file the information required by irc 6046. The irs issued a levy notice to farhy seeking to collect the section 6038 (b) penalties it had assessed for the tax years at issue. These penalties may apply to each required form 5471 on an annual basis. Web this practice unit provides an overview of usps that are required to file form 5471 under irc § 6038, and addresses the monetary penalties that apply under irc § 6038 when a usp fails to file a form 5471, files a form 5471 late, or files a form 5471 that is substantially incomplete. Citizens and residents who are officers, directors, or shareholders in certain foreign corporations file form 5471 and schedules to satisfy the reporting requirements of sections 6038 and 6046, and the related regulations. Current revision form 5471 pdf instructions for form 5471 ( print version pdf) recent developments Web (8) irm 20.1.9.3.5 (3) — clarified abatement policy for penalties systemically assessed when a form 5471 is attached to a late filed form 1120 or form 1065. Web failure to file information required by section 6046 and the related regulations (form 5471 and schedule o).

(9) irm 20.1.9.4.4 — updated to account for the repeal of irc 902, which was part of the tax cuts and jobs act. Web failure to timely file a form 5471 or form 8865 is generally subject to a $10,000 penalty per information return, plus an additional $10,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, up to a maximum of $60,000 per return. Web in response to the taxpayer’s failure to file forms 5471, the irs imposed $10,000 per year in initial penalties under section 6038 (b) and $50,000 per year in continuation penalties for the tax years 2003 through 2010. Web the maximum continuation penalty per form 5471 is $50,000. Tax court today held that the irs did not have statutory authority to assess penalties under section 6038 (b) against a taxpayer who willfully failed to file form 5471, information return of u.s. This also includes us taxpayers who have unreported foreign entities — such as foreign corporations, partnerships, and trusts. Web this practice unit provides an overview of usps that are required to file form 5471 under irc § 6038, and addresses the monetary penalties that apply under irc § 6038 when a usp fails to file a form 5471, files a form 5471 late, or files a form 5471 that is substantially incomplete. The internal revenue service continues to aggressively enforce noncompliance issues involving taxpayers with unreported foreign accounts, assets, investments, and income. The irs issued a levy notice to farhy seeking to collect the section 6038 (b) penalties it had assessed for the tax years at issue. Citizens and residents who are officers, directors, or shareholders in certain foreign corporations file form 5471 and schedules to satisfy the reporting requirements of sections 6038 and 6046, and the related regulations.

Citizens and residents who are officers, directors, or shareholders in certain foreign corporations file form 5471 and schedules to satisfy the reporting requirements of sections 6038 and 6046, and the related regulations. Tax court today held that the irs did not have statutory authority to assess penalties under section 6038 (b) against a taxpayer who willfully failed to file form 5471, information return of u.s. Web (8) irm 20.1.9.3.5 (3) — clarified abatement policy for penalties systemically assessed when a form 5471 is attached to a late filed form 1120 or form 1065. Web failure to timely file a form 5471 or form 8865 is generally subject to a $10,000 penalty per information return, plus an additional $10,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, up to a maximum of $60,000 per return. This also includes us taxpayers who have unreported foreign entities — such as foreign corporations, partnerships, and trusts. Web the maximum continuation penalty per form 5471 is $50,000. Current revision form 5471 pdf instructions for form 5471 ( print version pdf) recent developments (9) irm 20.1.9.4.4 — updated to account for the repeal of irc 902, which was part of the tax cuts and jobs act. These penalties may apply to each required form 5471 on an annual basis. Web this practice unit provides an overview of usps that are required to file form 5471 under irc § 6038, and addresses the monetary penalties that apply under irc § 6038 when a usp fails to file a form 5471, files a form 5471 late, or files a form 5471 that is substantially incomplete.

International Tax Forms When to File a Form 5471/5472, Penalties for

Web in response to the taxpayer’s failure to file forms 5471, the irs imposed $10,000 per year in initial penalties under section 6038 (b) and $50,000 per year in continuation penalties for the tax years 2003 through 2010. Citizens and residents who are officers, directors, or shareholders in certain foreign corporations file form 5471 and schedules to satisfy the reporting.

Are IRS Assessed Foreign Information Reporting Penalties Associated

The internal revenue service continues to aggressively enforce noncompliance issues involving taxpayers with unreported foreign accounts, assets, investments, and income. Criminal penalties may also apply for failure to file the information required by irc 6046. These penalties may apply to each required form 5471 on an annual basis. The irs issued a levy notice to farhy seeking to collect the.

A Dive into the New Form 5471 Categories of Filers and the Schedule R

Web failure to file information required by section 6046 and the related regulations (form 5471 and schedule o). Web (8) irm 20.1.9.3.5 (3) — clarified abatement policy for penalties systemically assessed when a form 5471 is attached to a late filed form 1120 or form 1065. Web in response to the taxpayer’s failure to file forms 5471, the irs imposed.

Want to Contest Penalties Associated with Forms 5471 or 3520 before the

Web failure to timely file a form 5471 or form 8865 is generally subject to a $10,000 penalty per information return, plus an additional $10,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, up to a maximum of $60,000 per return. Web in response to the taxpayer’s failure to file.

FORM 5471 TOP 6 REPORTING CHALLENGES Expat Tax Professionals

Current revision form 5471 pdf instructions for form 5471 ( print version pdf) recent developments Web failure to timely file a form 5471 or form 8865 is generally subject to a $10,000 penalty per information return, plus an additional $10,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, up to.

2018 Form IRS 5471 Fill Online, Printable, Fillable, Blank PDFfiller

Web in response to the taxpayer’s failure to file forms 5471, the irs imposed $10,000 per year in initial penalties under section 6038 (b) and $50,000 per year in continuation penalties for the tax years 2003 through 2010. Web (8) irm 20.1.9.3.5 (3) — clarified abatement policy for penalties systemically assessed when a form 5471 is attached to a late.

REASONABLE RELIANCE DEFENSE AGAINST 5471 PENALTIES Expat Tax

Criminal penalties may also apply for failure to file the information required by irc 6046. The internal revenue service continues to aggressively enforce noncompliance issues involving taxpayers with unreported foreign accounts, assets, investments, and income. Web in response to the taxpayer’s failure to file forms 5471, the irs imposed $10,000 per year in initial penalties under section 6038 (b) and.

Should You File a Form 5471 or Form 5472? Asena Advisors

The irs issued a levy notice to farhy seeking to collect the section 6038 (b) penalties it had assessed for the tax years at issue. Web this practice unit provides an overview of usps that are required to file form 5471 under irc § 6038, and addresses the monetary penalties that apply under irc § 6038 when a usp fails.

IRS Issues Updated New Form 5471 What's New?

Citizens and residents who are officers, directors, or shareholders in certain foreign corporations file form 5471 and schedules to satisfy the reporting requirements of sections 6038 and 6046, and the related regulations. These penalties may apply to each required form 5471 on an annual basis. Web the maximum continuation penalty per form 5471 is $50,000. Current revision form 5471 pdf.

IRS Form 5471 Carries Heavy Penalties and Consequences

The irs issued a levy notice to farhy seeking to collect the section 6038 (b) penalties it had assessed for the tax years at issue. Current revision form 5471 pdf instructions for form 5471 ( print version pdf) recent developments These penalties may apply to each required form 5471 on an annual basis. Web the maximum continuation penalty per form.

(9) Irm 20.1.9.4.4 — Updated To Account For The Repeal Of Irc 902, Which Was Part Of The Tax Cuts And Jobs Act.

Web failure to timely file a form 5471 or form 8865 is generally subject to a $10,000 penalty per information return, plus an additional $10,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, up to a maximum of $60,000 per return. Citizens and residents who are officers, directors, or shareholders in certain foreign corporations file form 5471 and schedules to satisfy the reporting requirements of sections 6038 and 6046, and the related regulations. Web (8) irm 20.1.9.3.5 (3) — clarified abatement policy for penalties systemically assessed when a form 5471 is attached to a late filed form 1120 or form 1065. Any person who fails to file or report all of the information requested by section 6046 is subject to a $10,000 penalty for each.

Tax Court Today Held That The Irs Did Not Have Statutory Authority To Assess Penalties Under Section 6038 (B) Against A Taxpayer Who Willfully Failed To File Form 5471, Information Return Of U.s.

Web in response to the taxpayer’s failure to file forms 5471, the irs imposed $10,000 per year in initial penalties under section 6038 (b) and $50,000 per year in continuation penalties for the tax years 2003 through 2010. These penalties may apply to each required form 5471 on an annual basis. This also includes us taxpayers who have unreported foreign entities — such as foreign corporations, partnerships, and trusts. Web failure to file information required by section 6046 and the related regulations (form 5471 and schedule o).

Web This Practice Unit Provides An Overview Of Usps That Are Required To File Form 5471 Under Irc § 6038, And Addresses The Monetary Penalties That Apply Under Irc § 6038 When A Usp Fails To File A Form 5471, Files A Form 5471 Late, Or Files A Form 5471 That Is Substantially Incomplete.

The irs issued a levy notice to farhy seeking to collect the section 6038 (b) penalties it had assessed for the tax years at issue. Current revision form 5471 pdf instructions for form 5471 ( print version pdf) recent developments The internal revenue service continues to aggressively enforce noncompliance issues involving taxpayers with unreported foreign accounts, assets, investments, and income. Criminal penalties may also apply for failure to file the information required by irc 6046.